Semester 2 Summary

This semester I started to try and make a portfolio risk management application in the same manner as the natural language application I did last semester. I started by researching about current methods used for portfolio management in R and how they could be used to optimize a portfolio. I decided that the main theory I wanted to focus on was the Modern portfolio Theory developed by Harry Markowitz, this plots the risk of an investment against the expected rate of return. However, I ran into some problems when developing the application relating to using real time data in the application.

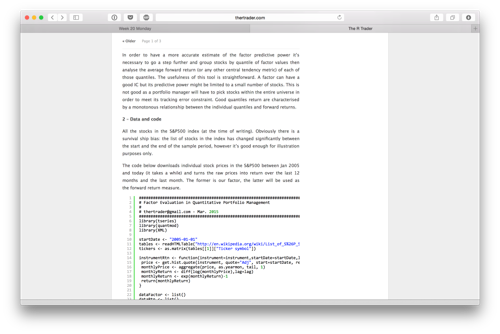

I then turned to learning about different uses of data science in finance, primarily in three areas: Portfolio Management, Pairs Trading, and Econometrics. Of the three, I was most familiar with econometrics since I had taken some classes on the subject previously. I started experimenting with the three subjects and wrote down the things that I did (that worked) in a script. Most of the things I did were graphs and analysis on hypothetical scenarios in a selected time frame since dealing with live data is more difficult.

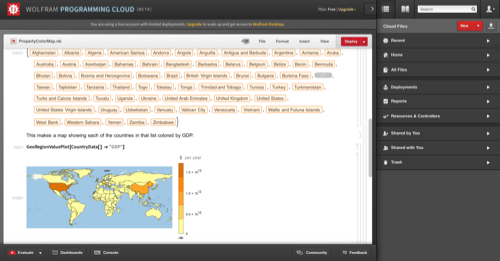

Towards the end of the semester I started to look into other dana science tools that relate to finance and I stumbled upon the Wolfram Language. I used the free cloud interface to try out if it is something that I would want to use in the future and I was very impressed with the features. Overall this semester was quite informative.